The era of monetary dominance is over. Helicopter money signals investment regime changes ahead.

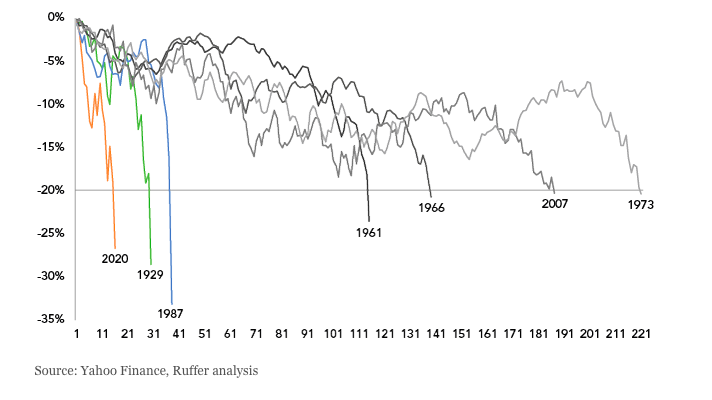

S&P performance until surpassing -20% threshold, number of trading days

It was the avalanche we have long feared. From record peak to bear market, the S&P fell faster during the ‘corona crash’ than ever before, as this month’s chart shows.

At peak turmoil, conventional offsets (bonds, gold) proved flaky friends: investors sold what they could, not what they perhaps should. Specialist crash protections allowed Ruffer portfolios to hold their ground.

The virus is especially dangerous for those with underlying conditions. History’s longest bull market – living on a glut of borrowed money and time – was one such victim. The era of monetary policy supremacy is another. For long-term investors, this is game-changing.