He may be one of only a handful of senior-ranking Ministers in Downing Street to have avoided catching Covid-19 but the pandemic has left the Chancellor of the Exchequer with a fiscal headache.

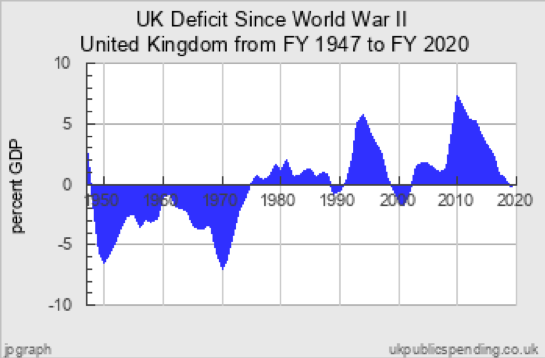

The last time the UK debt was bigger than the output of the economy itself was in the second world war. It took the iron determination of Sir Stafford Cripps to impose genuine austerity on the country after the war, and to produce annual surpluses to pay down the debt that had been incurred. The scale on the chart opposite is not big enough to accommodate this year’s deficit at £300 billion – somewhere around 20 per cent of GDP.

A Government can normally only run a deficit if the markets are willing to lend to it, but for this crisis the Bank of England has taken powers to finance the deficit through monetary financing – printing money for the Government instead. The Bank is already significantly expanding the money supply by purchasing bonds in the secondary market (the QE programme) and it will have to keep half an eye on the consequences of these operations for sterling and for inflation.

With the monetary accelerator pressed firmly to the floor – and after a massive Covid-19-related fiscal expansion – confidence in Mr Sunak’s running of the British economy will soon depend on his finding the public spending brake pedal. He will be announcing the results of his fundamental spending review this Autumn, setting out expenditure totals for each government department for the following three years. Then a Budget is due to take place in November, when he will be looking for new sources of revenue too.