Inflation is skyrocketing in practically the entire world. Central banks are getting scared and beginning to announce the end of expansionary measures, also known as tapering.

Why do central banks find themselves in a dilemma? Why has inflation risen so much? What is a bottleneck? What does tapering mean and how could it affect us? The objective of this article is to answer these, and other, questions.

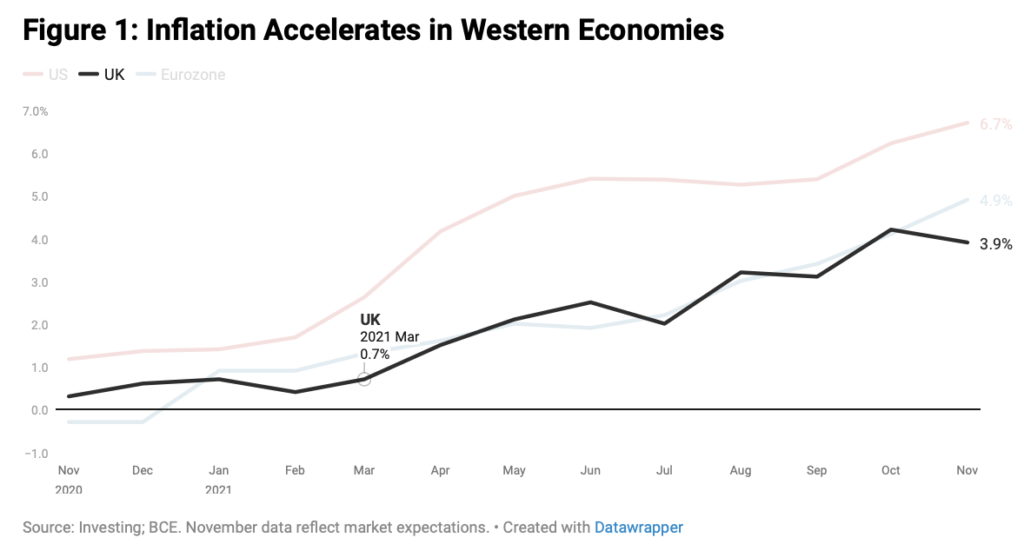

Inflation skyrocketing around the world

Central banks have one explicit mandate: to maintain the purchasing power of money. This is the main goal of monetary policy. Another mandate of some central banks is to sustain the level of economic activity (and it could be argued that they all have this as an implicit goal).

In developed countries, central banks’ inflation target tends to be 2% and in developing countries it tends to be 4% (while central bankers assert that these targets maintain purchasing power, in reality they denote lost purchasing power). Inflation is clearly higher than the targets in most countries.

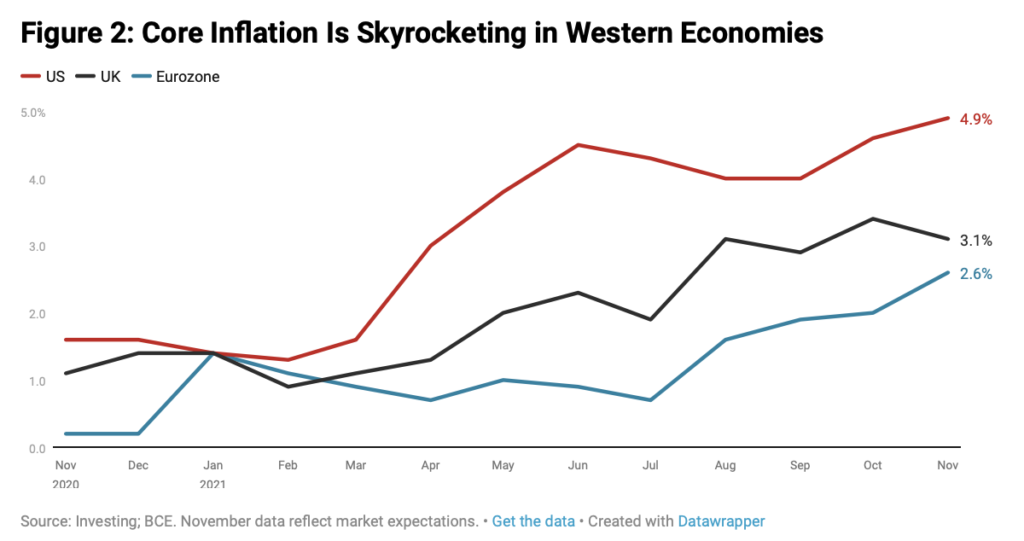

Core inflation (which excludes food and energy) is displaying a trend similar to that of general inflation, although core prices are growing somewhat slower than general prices.

Inflation and bottlenecks: what Is the real cause of inflation?

Most analysts attribute the inflation to bottlenecks. A bottleneck is what happens when a sector that lacks idle capacity and needs capital investments (including investments in human capital), which take time to bear fruit, has problems increasing production in the face of a sudden rise in demand.

But what has caused the bottlenecks? We see three factors:

- An increase in demand.

- A change in the makeup of demand.

- Production restrictions resulting from Covid 19.

Increases in demand

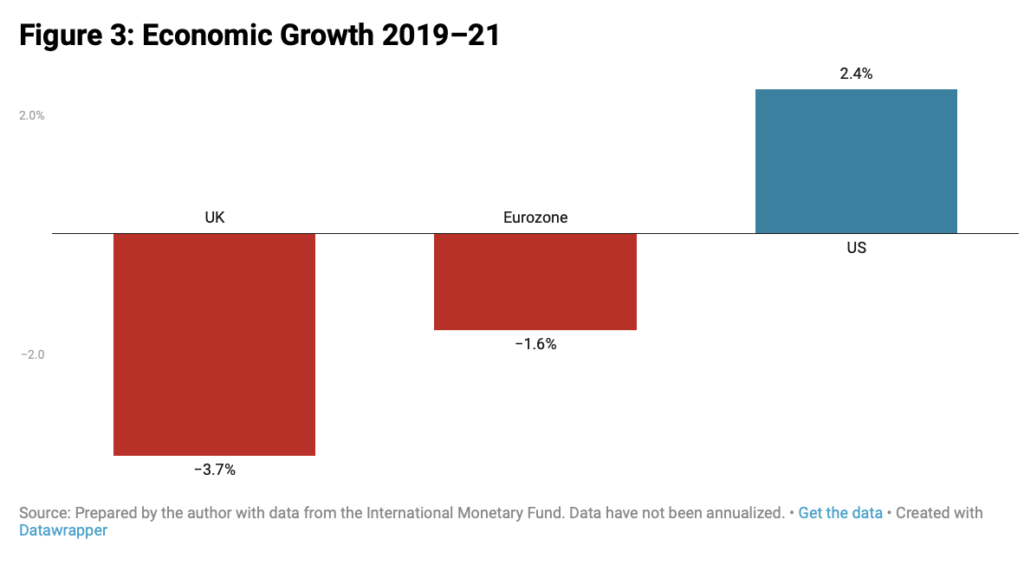

Many analysts consider the increase in demand to be a signal of economic recovery and of the global economy’s dynamism. A person’s ability to demand goods is usually predicated on their previous ability to sell or produce something of value (as Say’s law asserts). However, because of the pandemic, economic growth has been minimal or negative from 2019 to 2021 (for the economies analysed). Accordingly, this enormous increase in demand cannot be an indicator of prosperity.

In fact, in the US, the country with the best economic performance, private income did not rise to its prepandemic level until May 2021 and it is currently almost as low as that in February 2020. What has increased significantly – and thus increased demand and caused bottlenecks – is government transfers.