It’s more than a case of semantics

Deglobalisation, as a concept, has been mentioned quite a bit recently (along with the topics of onshoring and nearshoring), but the evidence of it happening on a significant scale thus far is scant, at best. Instead, key economic pointers suggest that, rather than going into reverse, globalisation has taken a breather – a trend that is best described as ‘slowbalisation’.

That said, it’s important to keep in mind that real estate is intensely local and even small shifts in cross-border trends can have an outsized impact on specific local real estate markets (think Brexit relocations and the ramification that’s had on Dublin, Luxembourg, Paris and Frankfurt). So, a better way to gauge slowbalisation is by looking at the two main transmission mechanisms of slowing globalisation for real estate: capital flows and the supply chain of goods.

Real estate capital flows

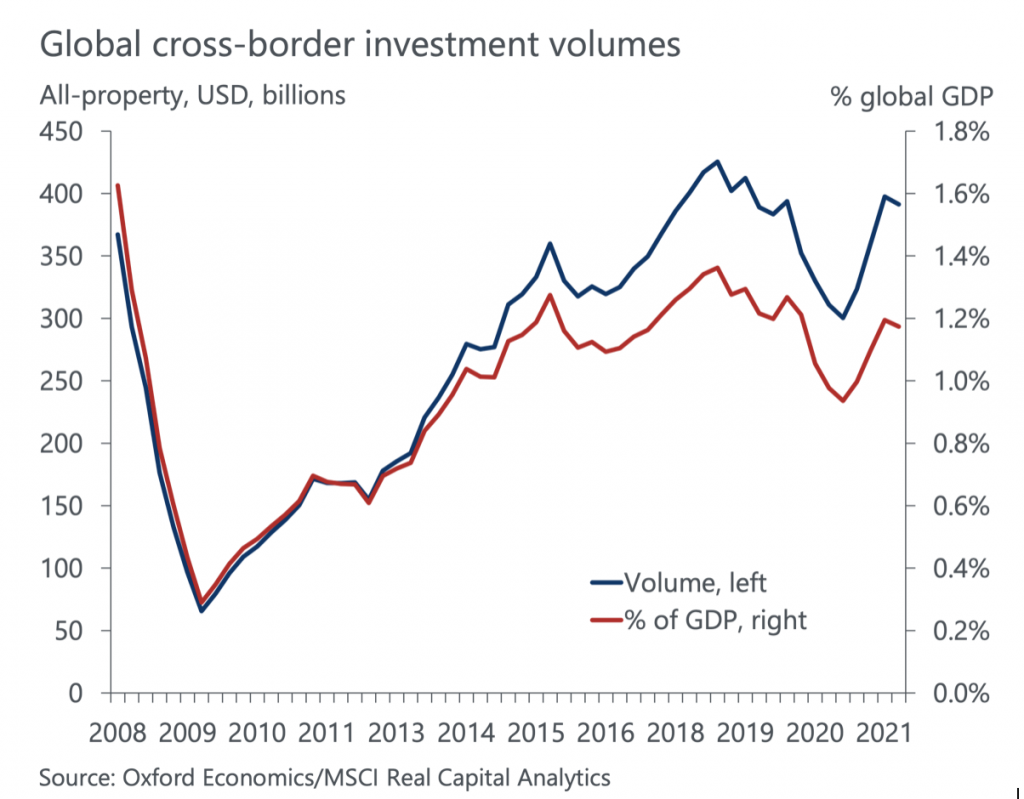

There’s little evidence to suggest that deglobalisation is occurring for real estate capital flows, but slowbalisation has been with us since 2014-2015. Although global cross-border investment returned to strength in 2021, reaching a three-year high at just under $400bn and logging its second-best year since records began in 2008, the flow of capital as a share of GDP was below 2018-2019, continuing the stationary trend that’s been in place since 2014-2015 (see chart). Indeed, global cross-border investment as a share of total volumes was the same in Q4 2021 as in Q1 2014.

Looking at the UK, we see a similar picture, with the share of the UK commercial property market owned by overseas investors flattening out since 2017 and while that levelling could be due to idiosyncratic factors such as Brexit or the pandemic impact, it is consistent with the global trend.