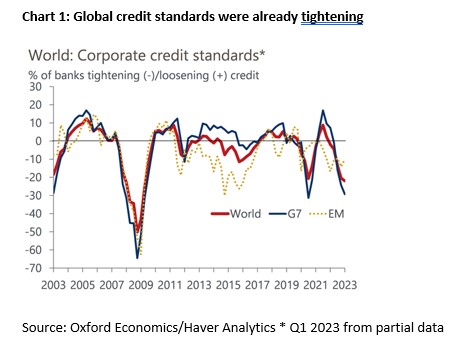

Global credit standards are set to tighten further in response to the recent bank funding turmoil, as suggested by movements in bank share prices and financial conditions during the aftermath of the Silicon Valley Bank (SVB) collapse and Credit Suisse takeover. The Oxford Economics indicator of global bank credit standards was the tightest reading in Q1 2023 since 2009, but was still well short of that seen at the worst point in the global financial crisis (Chart 1), implying that actual credit flows would turn negative in early 2024.

Under the Basel III framework, commercial real estate (CRE) loans typically hold higher risk weighting ratios than other segments of bank lending, which exposes the sector to a more marked pullback in lending should banks capital adequacy come under pressure. Given the poor market conditions, falling real estate values, and higher debt servicing costs, many CRE loans are likely to be reclassified with even higher risk weightings moving forward. This will require banks to hold more equity against the loans, both diminishing returns and disincentivising banks from providing additional credit to the sector, particularly as loan quality deteriorates, further exacerbating the tightening in credit to CRE.