Once a month we will bring you an interesting chart with a short commentary. Our aim is to illuminate the corners of financial markets.

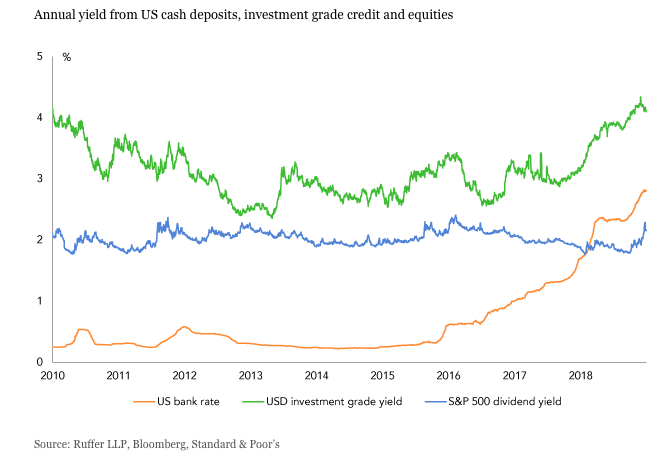

TINA turning?

Rising returns on cash may cause investors to withdraw from riskier assets such as equities and corporate bonds

Ever since the authorities cut interest rates around the globe to zero (or near zero) in the aftermath of the credit crisis there has been a strong incentive for savers to hold risky assets. With cash in the bank effectively yielding nothing, savers seeking any income were forced to buy riskier assets, predominantly equities and corporate bonds. This became known as the TINA trade – as in ‘there is no alternative’ for investors seeking any sort of income from their savings.